@SlyFox

IF you used the Online software to file 2022, there is no "Forms Mode" in the online software, and no What If worksheet either.

That's why I said you need to use the desktop software.

Thus, if you want to attempt to use the What IF worksheet to predict next year's situation, you'd need to buy the 2022 desktop software, and install it on a full Windows (Rev 10 or higher) or MAC computer (OS Big Sur 11 or higher).

__________________

You could then download your Online data file and use that as the starting point.

Thing is, that if you had a state in your Online data file then Deluxe would probably be the minimum to buy, since you must install the state before you can open that Online datafile. If you buy the Deluxe from TTX, it will include one free state software download too.........but If you had more than one state in your Online datafile...then you have to buy the extra state(s) for another $45 each from within the program.

TurboTax® 2022-2023 CD/Download Tax Software for Desktop (intuit.com)

If you buy the Deluxe software from a 3rd party (like Amazon), it will be cheaper, but you have to be careful to buy the right Deluxe software, since it is sold in two versions, both with, and without the one free state software download. (Opinion: Don't buy the CD, buy a software download.).

Right now Deluxe 2022 is $70 from Amazon, and $80 directly from TurboTax with the one free state. Your choice as to whether it's worth it or not......and you do have to buy new softwae every year.

___________

And...and..and no, the What-if worksheet does not predict anything about what the state taxes will be.

______

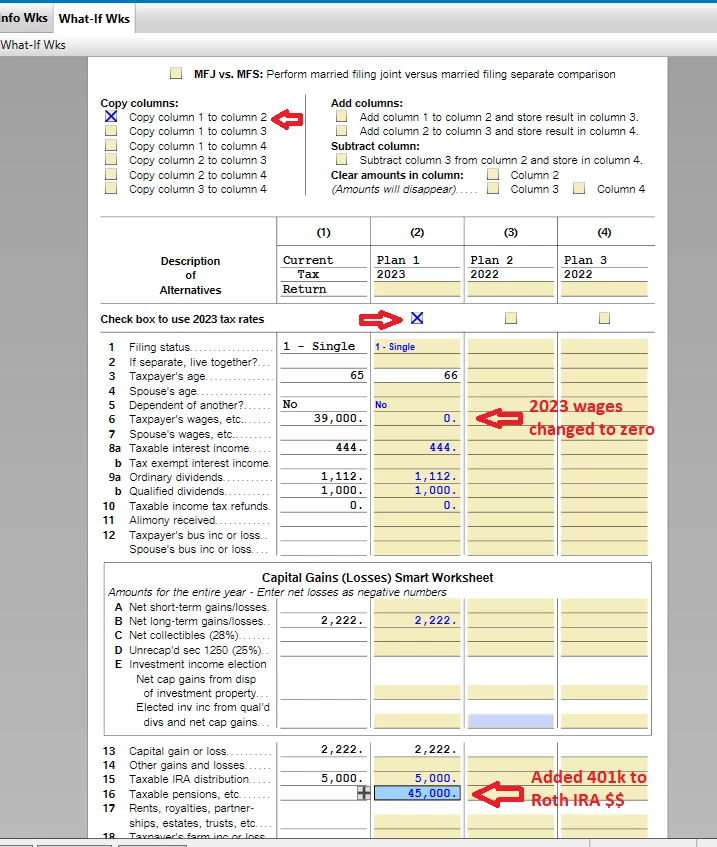

Here's a picture (down below) of just the top part of the What If Worksheet for a Single person who was age 65 in 2022, and will be 66 in 2023.......but it goes on with some 72 lines of details you can change as needed (or some more lines if you use itemized deductions) with the calculated tax assessed on line 62 (lines 63-to-71 deal with various credits or taxes you might have withheld/prepaid).

You will have to plan to spend a few hours looking at all the lines to decide which need to be changed and to understand where everything is.

(Sometimes it's simpler to guesstimate...like if you had wages of $45,000 in 2022, and replace that with $45,000 of Traditional 401k-to-RothIRA conversion, and everything else the same (No pension?), your Federal tax liability will be about the same .....liability being the total tax assessed before considering any withholding or estimated tax payments.)