- Community

- Topics

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

- Community

- :

- Discussions

- :

- Taxes

- :

- Retirement

- :

- Re: ira situation

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

i turned 70and a half this past year so my question is if i am still working and my spouse is in retirement and receives a pension can we claim a deduction for an IRA, if so how much?

Topics:

posted

March 1, 2020

7:42 PM

last updated

March 01, 2020

7:42 PM

Connect with an expert

Do you have an Intuit account?

You'll need to sign in or create an account to connect with an expert.

1 Best answer

Accepted Solutions

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

The RMD age change under the SECURE Act only applies to those reaching age 70½ after 2019.

Yes, your wife can contribute to an IRA based on your compensation as long and you file a joint tax return. If the contribution is for 2019 she must also be under age 70½; for contributions for 2020 and beyond there is no age limit. Whether or not a contribution to a traditional IRA will be deductible will depend on your modified AGI for the purpose and whether or not you yourself are covered by a workplace retirement plan.

March 1, 2020

9:38 PM

13 Replies

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

@jm789op wrote:

i turned 70and a half this past year so my question is if i am still working and my spouse is in retirement and receives a pension can we claim a deduction for an IRA, if so how much?

You should be aware that the SECURE Act signing into law in December that went into effect on Jan 1 2020 raised the age to take the first RMD from 70 1/2 to 72 AND removed the upper age limit to contribute to an IRA as long as you have sufficient taxable compensation to contribute.

The legislation itself covered many unrelated things and is lengthy to read, but Fidelity gave a simplified breakdown

The maximum IRA contributions for 2019 is $6,000, or $7,000 if you’re age 50 or older by the end of the year; or your taxable compensation for the year which ever is less.

(Taxable compensation is generally wages that you worked for - W-2 or net self-employed income minus the deducible part of the SE tax, but can include commissions, alimony and separate maintenance, and nontaxable combat pay ).

See IRS Pub 590A "What is compensation" for details:

https://www.irs.gov/publications/p590a#en_US_2018_publink1000230355

See this IRS link for Traditional IRA deduction limits when covered by a retirement plan at work.

https://www.irs.gov/Retirement-Plans/IRA-Deduction-Limits

**Disclaimer: This post is for discussion purposes only and is NOT tax advice. The author takes no responsibility for the accuracy of any information in this post.**

March 1, 2020

7:57 PM

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

The RMD age change under the SECURE Act only applies to those reaching age 70½ after 2019.

Yes, your wife can contribute to an IRA based on your compensation as long and you file a joint tax return. If the contribution is for 2019 she must also be under age 70½; for contributions for 2020 and beyond there is no age limit. Whether or not a contribution to a traditional IRA will be deductible will depend on your modified AGI for the purpose and whether or not you yourself are covered by a workplace retirement plan.

March 1, 2020

9:38 PM

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

I know. When I read it (70and a half) I only saw the 70 (I guess I am used to seeing it 70 1/2).

**Disclaimer: This post is for discussion purposes only and is NOT tax advice. The author takes no responsibility for the accuracy of any information in this post.**

March 1, 2020

9:48 PM

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

So in summary: if I'm working and I'm covered by a retirement plan and i turned 701/2 in 2019 and my spouse who is retread and receives no compensation except for their social security and pension, then they cannot take the IRA deduction.

March 2, 2020

8:41 AM

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

@jm789op wrote:

So in summary: if I'm working and I'm covered by a retirement plan and i turned 701/2 in 2019 and my spouse who is retread and receives no compensation except for their social security and pension, then they cannot take the IRA deduction.

[Edited]

IRS Publication 590-A - https://www.irs.gov/pub/irs-pdf/p590a.pdf

Your spouse -

For 2019, if you file a joint return and your taxable compensation is less than that of your spouse, the most that can be contributed for the year to your IRA is the smaller of the following two amounts.

1. $6,000 ($7,000 if you are age 50 or older).

2. The total compensation includible in the gross income of both you and your spouse for the year, reduced by the following two amounts.

a. Your spouse's IRA contribution for the year to a traditional IRA.

b. Any contributions for the year to a Roth IRA on behalf of your spouse.

March 2, 2020

8:53 AM

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

@jm789op wrote:

So in summary: if I'm working and I'm covered by a retirement plan and i turned 701/2 in 2019 and my spouse who is retread and receives no compensation except for their social security and pension, then they cannot take the IRA deduction.

Not correct.

*You* cannot contribute to a Traditional IRA at all for 2019. Your spouse (if under age 70 1/2) can contribute as long as the taxable compensation on a joint return to support the contribution.

Whether it will be deductible or not depends on the MAGI on the joint return. For married filing jointly and the spouse is covered by a retirement plan at work then the spouses Traditional IRA contribution will be fully deductible if your joint MAGI is $193,000 or less. Above that it phases out and becomes total not deductible with a MAGO of $203.000 or more. See the IRS publication below for details.

| The maximum IRA contributions for 2019 is $6,000, or $7,000 if you’re age 50 or older by the end of the year; or your taxable compensation for the year which ever is less. See this IRS link for Traditional IRA deduction limits when covered by a retirement plan at work. https://www.irs.gov/Retirement-Plans/IRA-Deduction-Limits |

**Disclaimer: This post is for discussion purposes only and is NOT tax advice. The author takes no responsibility for the accuracy of any information in this post.**

March 2, 2020

8:54 AM

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

As stated above by demertz, if your spouse is under 70 1/2, and you worked in 2019, she can contribute.

Kay Bailey Hutchison Spousal IRA Limit

For 2019, if you file a joint return and your taxable compensation is less than that of your spouse, the most that can be contributed for the year to your IRA is the smaller of the following two amounts.

- $6,000 ($7,000 if you are age 50 or older).

- The total compensation includible in the gross income of both you and your spouse for the year, reduced by the following two amounts.

- Your spouse's IRA contribution for the year to a traditional IRA.

- Any contributions for the year to a Roth IRA on behalf of your spouse.

This means that the total combined contributions that can be made for the year to your IRA and your spouse's IRA can be as much as $12,000 ($13,000 if only one of you is age 50 or older, or $14,000 if both of you are age 50 or older).

Your spouse (if under age 70 1/2) can contribute as long as the taxable compensation (from work) on a joint return to support the contribution.

[Edited 3/3/2020|5:16PM EST]

March 2, 2020

8:54 AM

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

@DoninGA The $103,000 is if *you* are covered by a retirement plan, the limit for a spouse that is not covered is $193.000.

**Disclaimer: This post is for discussion purposes only and is NOT tax advice. The author takes no responsibility for the accuracy of any information in this post.**

March 2, 2020

8:59 AM

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

Right...Thanks, I knew that. The grey cells must have been confused. Ughhhh.😬

March 2, 2020

9:01 AM

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

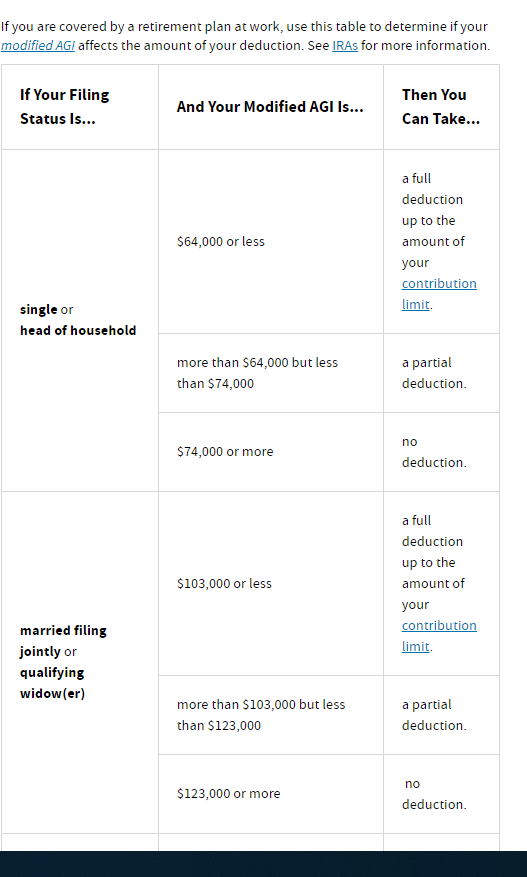

ira situation

IRA deduction limits 2019

March 9, 2020

7:02 AM

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

I don't think TurboTax is working correctly for my IRA deduction.

My wife and I are filing jointly and we want to max out our deductions. Our AGI is under $196,000

We are both 64. I am retired and getting a pension, but returned to work this past year and I am contributing to a 401(k) at work.

She has never worked outside the home.

We both have IRA's and I plan on maxing out at $7,000 each in our traditional IRA's.

After reading the deduction rules, I do not believe we should get a $14,000 deduction because 1) My W-2 clearly shows that I am contributing to a 401(k) and on top of that, 2) I am drawing a retirement pension.

But TurbTax is allowing a full $14,000 deduction. Is this correct?

February 8, 2021

6:58 PM

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

@LuvmyEllie wrote:

I don't think TurboTax is working correctly for my IRA deduction.

My wife and I are filing jointly and we want to max out our deductions. Our AGI is under $196,000

We are both 64. I am retired and getting a pension, but returned to work this past year and I am contributing to a 401(k) at work.

She has never worked outside the home.

We both have IRA's and I plan on maxing out at $7,000 each in our traditional IRA's.

After reading the deduction rules, I do not believe we should get a $14,000 deduction because 1) My W-2 clearly shows that I am contributing to a 401(k) and on top of that, 2) I am drawing a retirement pension.

But TurbTax is allowing a full $14,000 deduction. Is this correct?

If your MAGI is over $105K then you should only have a partial deduction. Your spouse should have a full deduction.

View the "Ira Deduction Worksheet" for the calculations that should answer your question. Something must have been entered wrong.

**Disclaimer: This post is for discussion purposes only and is NOT tax advice. The author takes no responsibility for the accuracy of any information in this post.**

February 8, 2021

7:22 PM

- Mark as New

- Bookmark

- Subscribe

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

ira situation

LuvmyEllie, your result suggests that you have not marked box 13 Retirement plan on TurboTax's W-2 form to match the marking of the box on the W-2 provided by your employer.

February 8, 2021

9:05 PM

Still have questions?

Questions are answered within a few hours on average.

Post a Question*Must create login to post

Unlock tailored help options in your account.

Get more help

Ask questions and learn more about your taxes and finances.

Related Content

turnips

Returning Member

snorkle

Returning Member

cuitcny

New Member

yacauwi

Level 1

sureshbk

Level 1