Question

1065 K1 Other Adjustments Notes Not Printing

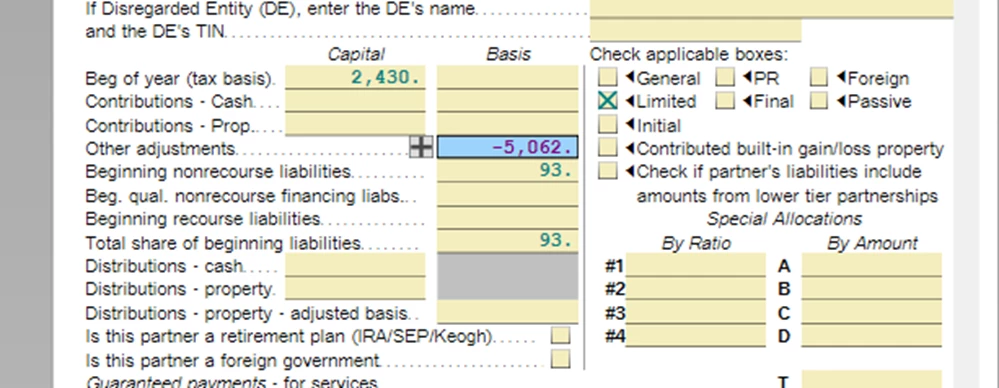

I have an LLC with 23 investors. I have added adjustments to the Basis using the Other Adjustments field on the K1 Worksheet.

When I print (or save to PDF) the K1 to PDF these adjustments are not printing on the K1 and the Notes are not printing as a separate page. There is a check box to check for the Note NOT to Print, but I have not checked it.

How do I get the adjustments and the notes to print both on the K1 Schedule L and as supplement notes?