Incorrect 8606 calculation

I am amending my 8606 for 2023 and I wonder if the 8606 calculation is wrong in TurboTax:

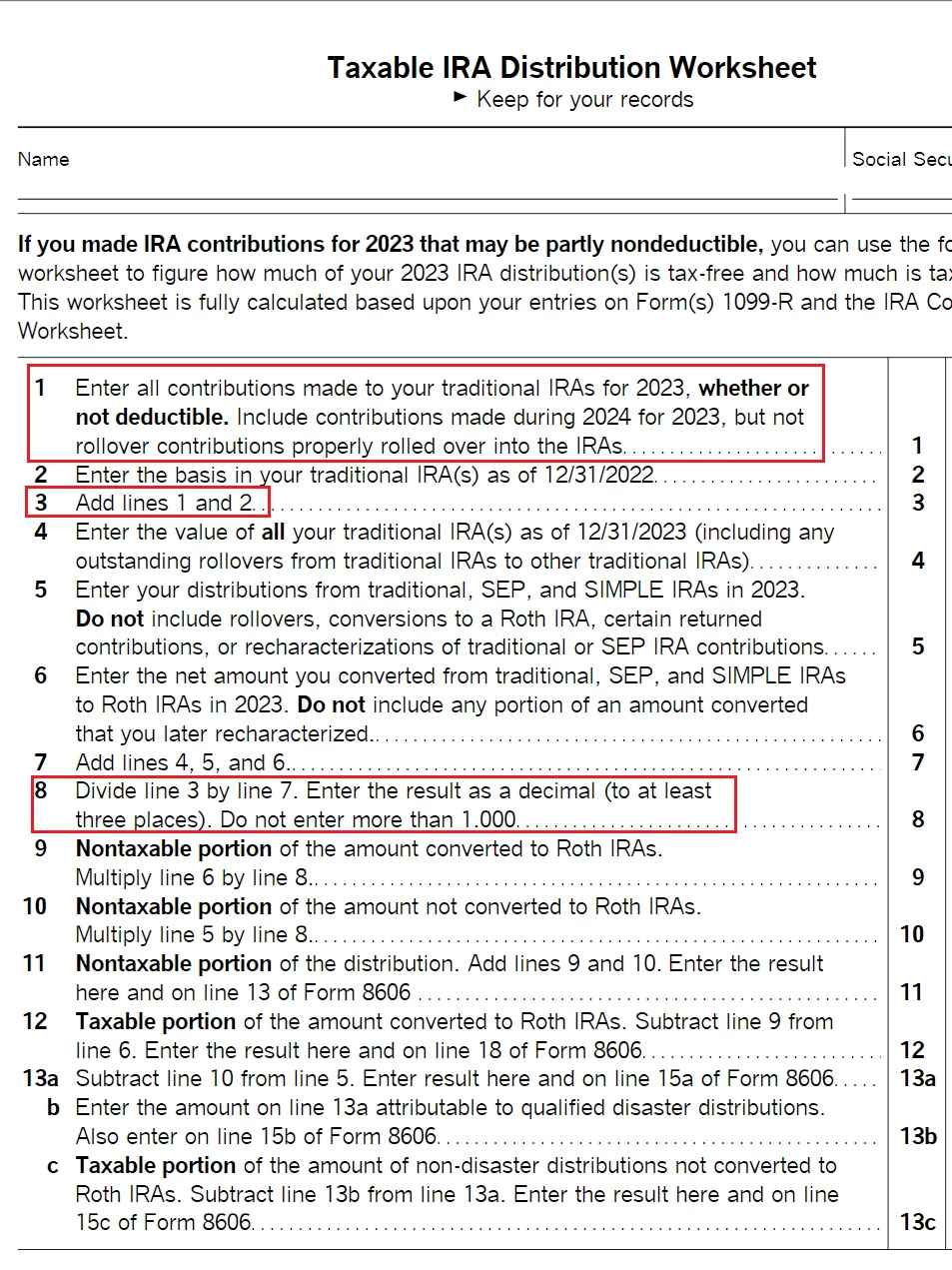

I made a late contribution to traditional IRA in Mar 2024 for 2023 backdoor. Previously I forgot to enter this $6500 in line 4 as I thought I made the contribution in 2023. So everything was wrong starting from line 9. After I entered $6500 in line 4, line 5 was correctly updated, but nothing was changed starting from line 9. IIUC, the line 5 change should affect line 10 which will affect all the following lines.

I noticed that in "Tax IRA Dist-T" worksheet which seems used by TurboTax internally to calculate 8606, it did not distinguish if the contribution I made is in 2023 or 2024. It may explain the reason why nothing was changed.

I am wondering if my understanding is correct. If so, how to fix this. If not, what did I misunderstand. Thank you!