Solved

Refund Decreased when I enter my 1099R

Why did my refund decrease when I entered my 1099R?

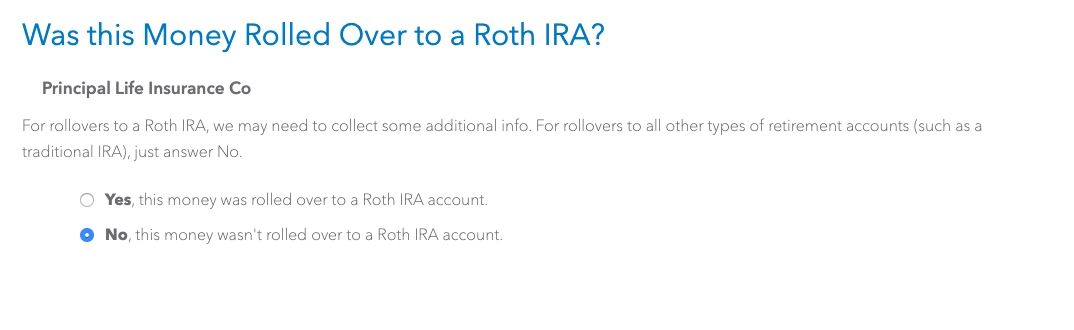

I rolled it over to a Roth IRA I didn't see any of that money. I'm just a little confused and I haven't filed yet because that seems wrong.

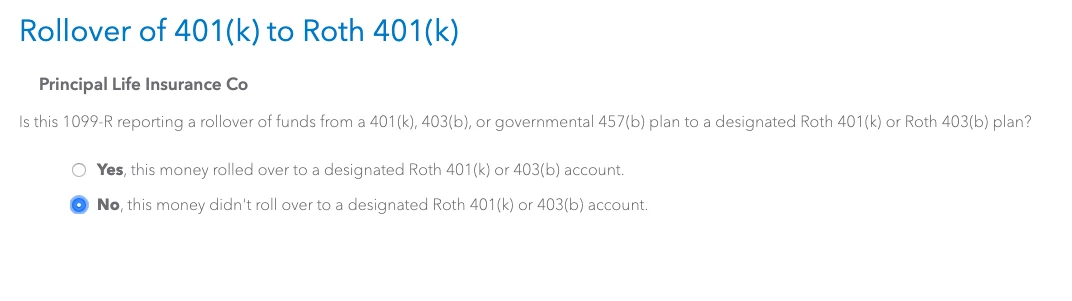

I noticed when I fill out all the information that matches the 1099R it asks me the following questions. (Note Distribution code is G)

Of course, when I answer truthfully, that it is reported and it did get rolled over to a Roth. The refund drops significantly.

I also noticed that if I change the Distribution code from G to H(This code just makes more sense to me) then it does not drop my refund, and doesn't ask me the questions above.

I really don't know what to do.

Do I need to report the rollover?