How to enter a 401-K distribution on a 1099-R Code E

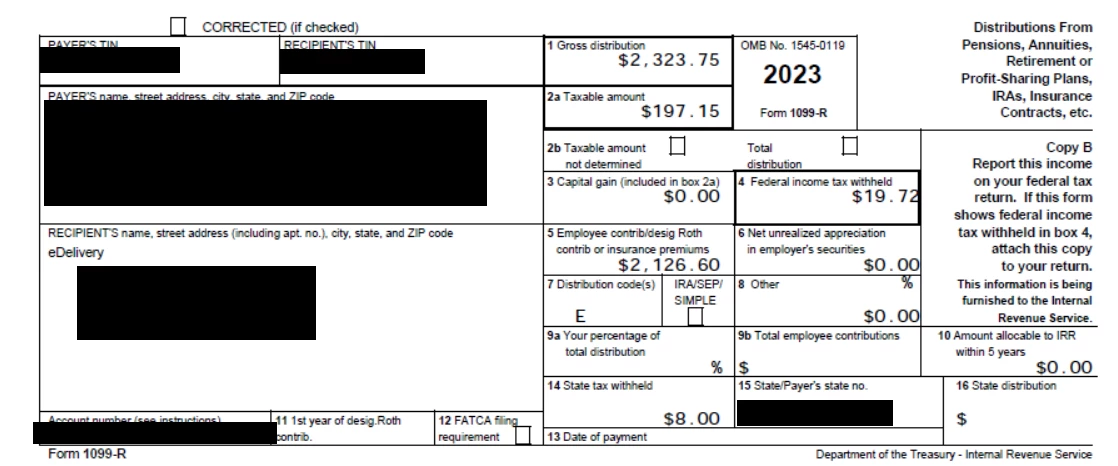

My employer offers a company savings plan that allows after-tax contributions, which can then be rolled into a Roth IRA. in 2023 I contributed too much to the plan. I received a 1099-R that has data in Box 1 (Gross Distribution), Box 2 (taxable amount), Box 5 (Employee contributions to a Roth), Box 7 Code E (Distributions under Empllyee Plans Compliance Resolution System), and box 14 (state tax withheld).

I also get a similar 1099-R with Code G, and the community has helped me with that. Based on my past experience, I think I have to enter the code E distribution into TurboTax as two 1099-Rs.

Would the first 1099-R show Box 1 of 2126.60 and Box 5 of 2126.60, with the the Box 7 distribution code be E?

Would the second 1099-R show $197.15 in Box 1, $197.15 in Box, 2, and Box 7 distirbution code of E. I'm believe the tax withheld (Box 4 and Box 14) would go with this 1099-R.

I input these numbers into TurboTax this way, and I got no errors. I just wanted to confirm I am doing it correctly, and have the tax withheld on the correct 1099-R.

I'm not clear on where the money actually went. I don't remember receiving a check from my 401-K holder for any of this. The same brokerage handles both my 401-K and the rollover Roth and conventional IRA. I would expect to at least have received a check for the $197.15 minus the taxes withheld. I think the $2126.60 went into a Roth. Did the 2126.60 go into my Roth account as a 2024 contribution, lowering how much I can contribute this year? My brokerage has been less than helpful.

Thanks for any explantions. I'm filing late due to K-1s & K-3s I get for one of my investments.