Cryptocurrency Guide

What is cryptocurrency?

Cryptocurrency is a medium of exchange, which provides:

A common unit of value, so things with differing values can be traded without needing to barter

A way to put a value on something intangible, like a service, and

A means of storing holding value

National governments typically have backed only their own fiat currency. Increasingly, governments are adopting CBDCs (see the Glossary of cryptocurrency terms section: fiat currency, CBDC).

Note: The IRS treats cryptocurrencies as properties for tax purposes.

All cryptocurrencies reside within a blockchain ecosystem, and can never reside anywhere else, like in a bank account. Contrast this with an online banking system’s money, which can be converted into hard currency and back, via ATM machines or bank tellers. A blockchain recordkeeping system has some potential benefits over a conventional central database regarding security, autonomy (meaning few or no intermediaries), transparency, and community consensus.

Because cryptocurrency exists only in electronic format, it is a digital currency governed by rules determined entirely by consensus among a virtual (online) community's members. For example, bitcoin resides on the Bitcoin blockchain and ethereum resides on the Ethereum Classic blockchain. In practical terms, virtual currency and digital currency are used interchangeably.

Common cryptocurrency concepts and terms

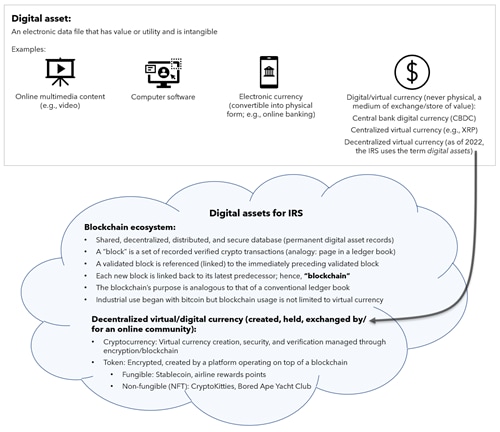

This diagram may help to clarify some of the terms used with cryptocurrency and digital assets.

Glossary of cryptocurrency terms

| airdrop | Free distribution of a nominal number of coins or <em>tokens</em> to multiple users to foster adoption of a new virtual currency |

| altcoin | Any <em>cryptocurrency</em> that is not <em>bitcoin</em> hence an “alternative coin” |

| API | Application Programming Interface: software enabling computers to work together. A language translator of sorts, for computers |

| bitcoin (cryptocurrency) | The first cryptocurrency, which at time of writing, was still dominant in the broader crypto ecosystem |

| Bitcoin (network) | The first <em>blockchain</em> |

| block | A data file containing all of the transactions made and validated during a specific time frame. Each new validated block is placed first among all blocks on that network, and is linked to its predecessor, forming a <em>blockchain</em> |

| blockchain | See the preceding definition of <em>block, and see the preceding </em>Section: <em>Cryptocurrency and digital assets</em> |

| CBDC | Central bank digital currency is: regulated solely by a country’s central bank/treasury (not decentralized). It’s intended as a digital replica of the country’s traditional fiat currency, and isn't restricted in supply like most <em>cryptocurrencies</em> |

| cold wallet | An offline <em>cryptocurrency</em> <em>wallet</em> or storage device for private <em>keys</em>. More secure but less convenient than an online <em>hot wallet</em> |

| consensus mechanism | A program used in blockchain systems to ensure data safety and integrity, and keep those with nefarious intentions locked out of distributed ledgers |

| cost basis | A tax term for the dollar value of a property at time of possession. Transaction costs of obtaining the property are included |

| cryptocurrency | See the preceding Section: <em>Cryptocurrency and digital assets</em> |

| cryptocurrency exchange | A platform where digital properties are bought, sold, and traded for <em>fiat currency</em> or other digital properties, somewhat like a conventional Dow Jones. Currently, Binance is the largest cryptocurrency exchange |

| decentralized | A decision-making and control model where a <em>blockchain </em>community's decisions are made by majority consensus among the blockchain's users. Unlike centralization, where a single entity has decision-making power and control |

| DAO | Decentralized Autonomous Organization: a “trustless” blockchain business model, governed by <em>smart contracts,</em> to avoid conventional “top down” organization structure and control |

| DeFi | Decentralized Finance: uses <em>smart contracts</em> on <em>peer-to-peer</em> <em>blockchain</em> networks to enable a variety of tokenized lending, trading or borrowing services without a central financier (bank) |

| delegation | Users in the community who can’t meet minimum <em>proof of stake mining</em> requirements can <em>stake</em> a lesser amount of <em>cryptocurrency,</em> to earn some staking rewards (similar to earning interest) while the community <strong>delegates</strong> the <em>validation</em> work to a proof of stake miner |

| deposit | <em>Cryptocurrency</em> sent to an account from an <em>exchange</em>, <em>wallet</em>, or custodian, often with a transaction <em>(gas)</em> fee charged by the <em>blockchain</em> network |

| digital assets | See the preceding Section: <em>Cryptocurrency and digital assets</em> |

| digital currency | See the preceding Section: <em>Cryptocurrency and digital assets</em> |

| distributed ledgers | Shared databases that record information that is networked for many users in different locations to access |

| ether | Ether (ETH) is the native <em>cryptocurrency</em> of the Ethereum blockchain, currently ranked second after <em>bitcoin</em> in price and market value |

| fiat currency | A medium of exchange, store of value, and unit of account issued and backed by a national government’s finances, rather than by a physical commodity (such as gold) |

| fork | After an update to a <em>blockchain</em>’s protocol, if some users don't agree to adopt the update, the blockchain is divided in two. See also <em>hard fork</em> and <em>soft fork</em>. |

| fungible | All units are identical, as with a commodity or a currency. A <em>cryptocurrency</em> (such as <em>bitcoin</em>) is fungible |

| gas fee | Strictly speaking, a fee for transactional use of the Ethereum <em>blockchain</em> network. Other blockchains may use terms such as transaction or miner fees. In practice, the term gas fees sometimes gets used to generically refer to any such fees |

| hard fork | A <em>fork</em> in which the old and new protocols are incompatible and users not adopting the update can’t interact with adopters. For example, bitcoin cash emerged from a Bitcoin hard fork |

| hot wallet | An online <em>wallet </em> |

| key | A long string of alphanumeric characters used for security in the blockchain ecosystem. See also <em>public key </em>and <em>private key</em> |

| mining | A process for validating and securing pending <em>cryptocurrency</em> transactions (by paid third party virtual community users- miners) before being recorded on the <em>blockchain</em>. See also<em> proof of stake </em>and <em>proof of work</em> |

| minting | N<em>on-fungible tokens</em> are minted onto the<em> blockchain </em>by a creator who'll connect to an NFT marketplace, upload the token to their <em>blockchain</em> of choice using a creation widget, specify any royalties via <em>smart contract</em>, pay applicable <em>fees, </em>then hold the NFT, or list it for sale |

| mobile wallet | A <em>wallet</em> app installed on a smartphone. Mobile wallets are typically <em>hot wallets</em> |

| node | A computer connected to a distributed <em>blockchain</em> network to serve various purposes such as <em>validation</em> of transactions, or observing activity on the blockchain |

| non-fungible token (NFT) | A unique (thus non-fungible) <em>token</em>,<em> </em>for proving ownership of a <em>digital asset</em> like an artwork, recording, virtual real estate or pet image. The use of NFTs is broadening to include <em>real world</em> assets like event tickets and limited-edition wines. Buy and sell transactions occur on NFT marketplaces such as OpenSea |

| peer to peer (P2P) | A <em>decentralized</em> network structure intended to work in the best interest of all parties involved, with no intermediary (bank or other institution) involvement |

| private key | Enables secure account access, and digital user ID for anonymous sign-in before performing any transaction, including “unlocking” of any <em>cryptocurrency</em> received |

| public address | Shortened version of a user’s<em> public key</em> that can receive transactions, similar in purpose to a bank account number |

| public key | A <em>key</em> enabling sending of cryptocurrency to a recipient user when paired to the recipient’s <em>private key</em> |

| proof of stake mining | A selected user will <em>stake</em> (ante up) a (usually) large amount of <em>cryptocurrency</em> for the right to <em>validate</em> and record a new <em>block</em>, and then receive a cryptocurrency staking reward, plus the return of their stake |

| proof of work mining | Miners use massive computing and electricity resources, competing to be the first to solve an epically detailed arithmetic puzzle. The winner then <em>validates</em> and records the pending <em>block</em>, and is paid in <em>cryptocurrency</em> |

| smart contract | An agreement that is coded, stored, secured and executed on the <em>blockchain</em>, visibly and irreversibly. It basically replaces conventional paper-based documents and legal intermediaries (lawyers, courts) |

| soft fork | A backwardly compatible <em>blockchain</em> software update. The new protocol can still “talk to” the old one. So, upgraded network <em>nodes</em> can still communicate with non-upgraded nodes |

| software wallet | Holds a user's <em>keys</em> (public or private) and secures their <em>cryptocurrency</em>. Typically an app on the user's desktop or mobile device, connected online |

| stablecoin | A type of fungible <em>token</em>, combining the benefits of <em>cryptocurrency</em> with the stability of cash, efficiently and economically. Often pegged to a stable <em>fiat currency</em>, or, may be stabilized by other <em>DeFi</em> means. Tether is currently the dominant stablecoin |

| staking- delegation | See <em>delegation</em> |

| staking- validation | See <em>proof of stake mining</em> |

| store of value | An asset that will likely keep its value over time, and can be reliably retrieved and exchanged in future, such as <em>fiat currency</em>, real estate, and rare metals such as gold and silver |

| token | A digital asset governed by a <em>smart contract, </em>enabling the<em> </em>transfer and storing of value on a <em>blockchain</em> network. Can be either <em>fungible</em> or <em>non-fungible</em> |

| validation | Verification and approval of a pending transaction by a user selected by the community, under the <em>blockchain’s</em> verification protocol |

| wallet | A device or service providing: storage for a user’s public and private <em>keys</em>, and an interface for <a href="https://turbotax.intuit.com/personal-taxes/crypto-taxes/">crypto</a> asset access |

How is cryptocurrency taxed?

Note: In this section, for simplicity, the term “cryptocurrency” is used as a catch-all for cryptocurrency, digital currency, virtual currency, tokens, NFT’s, digital assets. For more info on these and other terms, see the section covering Digital Assets. For information on “digital assets” for IRS federal tax purposes, see Digital Assets.

Depending on the situation, cryptocurrency is taxed as:

Ordinary income, if for example, it earns a return for the holder from an income stream (similar to interest) or

A capital gain or loss from a sale of property after its value has increased or decreased

If merely bought and held, it’s not taxed until something is done with it, such as disposal

See the sections that follow for answers to common questions around cryptocurrency and how it is taxed.

What are the capital gain and capital loss tax rules?

Most any property with a lasting use or value, like a home, car, stocks and bonds or cryptocurrency, is a capital property. When an investment property (such as a cryptocurrency) is sold, a capital gain results if the sale proceeds are more than the cost of the property when acquired, plus any transaction costs. If the proceeds are less, it’s a capital loss.

In the United States a capital gain or loss from a property held for:

One year or less is a short-term capital gain or loss

More than one year is a long-term capital gain or loss

Net long-term capital gain is: the long-term capital gains for the year less long-term capital losses including any unused long-term capital loss carried over from previous years.

Net capital gain is: the net long-term capital gain for the year less your net short-term capital loss for the year.

The tax rate applied to capital gains depends on one’s holding period (short or long term), taxable income, and filing status. Net short-term capital gains are taxed at the rate for ordinary income, and net long-term capital gains are taxed at specified rates. See more info at A Guide to the Capital Gains Tax Rate: Short-term vs. Long-term Capital Gains Taxes.

What is the cost basis of a capital property, including cryptocurrency?

The tax term for the cost of an investment property is cost basis. Like any investment property, the cost basis of cryptocurrency is the amount paid for it, including transaction fees, upon acquisition. Cryptocurrency can be received (and its cost basis established) in many ways. Some examples are when virtual currency is received:

As payment for having provided goods or services to someone

As wages from employment services

For no consideration (free)

From NFT royalties

From an airdrop

From mining or staking

From swapping for a previously held cryptocurrency

By purchasing it with fiat currency

Which cryptocurrency events result in capital gain or loss?

A capital gain or loss will result from the disposal of cryptocurrency:

As payment for goods or services received

In exchange for cash

In exchange for a different cryptocurrency

Capital losses are first used to offset capital gains of the same type. Short-term losses are first deducted against short-term gains, and long-term losses are deducted against long-term gains. Net losses of either type can then be deducted against the other kind of gain.

For example,

If one has $2,000 of short-term loss and only $1,000 of short-term gain, the net $1,000 short-term loss can be deducted against net long-term gain (assuming you have one)

If one has an overall net capital loss for the year, they can deduct up to $3,000 of that loss against other kinds of income, including salary and interest income

Any excess net capital loss can be carried over to future years, to be deducted against capital gains and against up to $3,000 of other kinds of income

If using married filing separate filing status, the annual net capital loss deduction limit is only $1,500

So, tracking and reporting these unused losses year to year for possible future use is important.

Why is cost basis so important, and what pitfalls must be avoided?

Having the correct cost basis is needed to determine the correct capital gain or loss amount, to report and pay the correct tax. So keeping records of all cryptocurrency deposits is really important.

Pitfall to avoid: a cryptocurrency can be moved from one virtual location (such as an exchange or wallet), to another location. The cost basis upon the initial acquisition is required for determining the correct capital gain or loss, if one needs to be reported at tax time. A subsequent wallet or exchange account (post-transfer) will likely not have a record of the initial cost upon the initial acquisition.

Example:

Jean bought one ExampleCoin on the Binance exchange in year 1, for $100 cash

In year 2, Jean transferred the ExampleCoin to a Coinbase exchange, when the value of one ExampleCoin was $200. Transfer between accounts isn’t a taxable event

In year 3, Jean sells the ExampleCoin for $300

The year-end report that Jean receives from Coinbase lists a cost basis of $200 for the one unit of ExampleCoin that was sold (the value of the ExampleCoin when it arrived at Coinbase)

Jean uses only a report from Coinbase and calculates an INCORRECT capital gain of:

$300 proceeds less $200 cost basis = capital gain of $100

In fact, the CORRECT capital gain is:

$300 proceeds less $100 cost basis (original cost) = capital gain of $200

Jean may eventually receive an enquiry from the IRS, asking if the capital gain has been under-reported by $100.

What is the importance of the choice of cost basis method?

If one holds two tokens of a cryptocurrency that were acquired at different points in time, they will likely not have the same cost basis. If a token is sold, what cost basis amount is used to calculate the capital gain or loss? Is it the first token (known as first in, first out, FIFO), the last one (last in first out LIFO), an average of the two cost bases (average cost basis ACB), the highest cost token (highest in first out HIFO), or by picking one (specific identification)?

The IRS allows specific identification. If specific identification isn't used, the IRS considers one to have used FIFO. Use of the same cost basis calculation method year-over-year is recommended so as to avoid double counting or missing any transactions.

As one's volume of disposal transactions increases, the required information gathering and calculations can become more daunting, exhausting and risky.

Using an automated cryptocurrency tax calculator is an option worth considering. One such option is described in the next section, What's Intelligent Tax Optimization?

How are various cryptocurrency types taxed?

Review the following sections for more information about how each type of cryptocurrency is taxed.

Is cryptocurrency mining taxed?

Cryptocurrency compensation received from proof of work mining or proof of stake mining:

From a business-like activity, is taxable as Business Income

From nonbusiness activity, is taxable as Other Income

How's the reward from staking delegation taxed?

When a reward is received from staking delegation, the tax treatment depends on the type of reward. If the reward is for:

Additional tokens, it's taxed as ordinary income

An increase in the value of tokens already held, it's taxed as a capital gain

How's a hard fork taxed?

A hard fork, on its own, isn't a taxable event. If the hard fork is followed by receipt of new tokens, the tokens are taxable as ordinary income based on the fair market value at the time of receipt.

How's an airdrop taxed?

Tokens received from an airdrop are taxable as ordinary income based on the fair market value at the time of receipt.

How are decentralized finance (DeFi) arrangements taxed?

DeFi tries to mirror financial services like lending, borrowing, and earning interest, on a blockchain with no intermediary such as a bank. Existing ordinary income and capital gains rules can be applied to basic DeFi transactions. Tax treatment of more specialized DeFi arrangements can be reviewed at Decentralized Finance (DeFi) is red hot, but what are the tax issues?

How are decentralized autonomous organizations (DAO) transactions taxed?

A DAO may initially raise capital by receiving fiat currency (money) in exchange for its native token. It may invest in assets if there is consensus of approval.

When cryptocurrency is received from a DAO in exchange for goods or services, or via promotion upon a DAO launch, the cryptocurrency received will generally be taxed as income, similar to the general case when there's no DAO involved, say, as payment received for goods and services provided, or from air drops.

How are stablecoin and NFTs taxed?

In 2022, the IRS clarified its position: cryptocurrency, stablecoin, and NFTs, are all digital assets, subject to the same tax treatment. See Digital Assets for more information.

Are there any nontaxable crypto events?

Yes, the following aren't taxable:

Cash purchase of cryptocurrency

Holding of cryptocurrency

Transfer of cryptocurrency between wallets

Receipt of cryptocurrency as a bonafide gift

Gifting of cryptocurrency within these limits:

Any gift amount under the $19,000 annual gift tax exclusion limit

Any gift amount over $19,000 but under the $13.99 million cumulative lifetime exclusion limit

For more information see Instructions for Form 709

Donating cryptocurrency to a charitable organization

Cryptocurrency transactions within a tax-deferred or tax-free account

When does a cryptocurrency exchange issue a form 1099-DA, 1099-K, or 1099-MISC?

1099 forms in general are intended for disclosing non-employment income. Currently with cryptocurrency there can be inconsistency in how and when the forms are used, and the completeness and accuracy of the information they contain. Note: Regardless of whether one receives a 1099 form, one is required to accurately report all cryptocurrency income to the IRS.

Form 1099-B was originally issued by traditional investment brokers and exchanges to report a client’s individual securities sales and the resulting gains or losses. Beginning with tax year 2023, its scope was expanded to include digital asset transactions as well. As part of this change, U.S.-based cryptocurrency exchanges are required to collect tax-reporting information from their customers so they can issue the appropriate 1099 forms to both the customer and the IRS.

Starting in 2025, Form 1099-DA will replace Form 1099-B for reporting digital asset activity. The 1099-DA provides potentially useful information for reporting cryptocurrency disposals, including cost basis. However, caution is advised—see the previous section, “Why is cost basis so important, and what pitfalls must be avoided?”

Form 1099-K shows the gross total of all transactions, both taxable, and nontaxable, on a given platform. For income tax purposes, each transaction needs to be reported.

Form 1099-K tracks income you made from selling goods or providing services via payment apps and online marketplaces. Examples include PayPal, Venmo, Square, Etsy, Uber, and eBay.

You should receive a 1099-K if you made more than $20,000 and the number of transactions exceeds 200 on one of these platforms.

Even if you don't receive a 1099-K, or you make less than $20,000, you still need to report all taxable income to the IRS.

Form 1099-K tells the IRS and the cryptocurrency investor that there's been potentially taxable cryptocurrency activity during the year. Taxable cryptocurrency transactions must be reported on the investor’s tax return regardless of whether a 1099-K has been issued.

Form 1099-MISC is issued to indicate total miscellaneous income. It's used by some cryptocurrency platforms to indicate other income of more than $600, from cryptocurrency staking, rewards and other sources of income. It doesn't disclose individual income transactions and it has no information about gains or losses. The individual income transactions must be imported or uploaded into the tax return software to be reported as either: other income if not self-employed, or as self-employment income if self-employed.

What if cryptocurrency is lost or stolen?

There's no available tax deduction for losses from lost or stolen cryptocurrency.

How do I enter cryptocurrency in TurboTax?

Intelligent Tax Optimization (ITO) is a crypto aggregator within the TurboTax application. It helps make cryptocurrency tax filing easier.

ITO is able to:

Connect to exchanges and wallets, and import transactions and tax forms

Identify taxable transactions

Calculate the cost basis values for transactions

Make remediation (filling any information gaps) easier

Here are some articles that will help you enter your crypto transactions in TurboTax: